Date: 23 July 2025

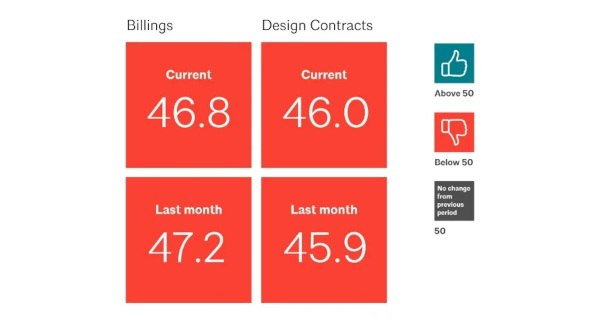

Inquiries into new projects increased for the second consecutive month and grew at the strongest pace since last fall with a score of 53.6, indicating clients are starting to send out RFPs and initiate conversations with architecture firms about potential projects after a lull since mid-winter. These inquiries do not necessarily translate into actual projects, as the value of newly signed design contracts declined for the 16th consecutive month in June. It is unlikely that firm billings will return to positive territory until the value of new design contracts also starts to increase again.

“Business conditions were soft nationwide in June, with a slight billing increase in the South for the first time since October,” said Kermit Baker, PhD, AIA Chief Economist. “Other regions saw declining billings, though at a slower pace. While all specializations experienced softer billings, the decline slowed for commercial/industrial and institutional firms. Multifamily firms faced the weakest conditions, with further declines.”

Key ABI highlights for June include:

• Regional averages: South (50.6); Northeast (46.5); Midwest (45.7); West (45.8)

• Sector index breakdown: institutional (49.2); commercial/industrial (47.4); mixed practice (firms that do not have at least half of their billings in any one other category) (45.5); multifamily residential (43.8)

• Project inquiries index: 53.6

• Design contracts index: 46.0

The regional and sector categories are calculated as three-month moving averages and may not always average out to the national score.

Access resources to help architects successfully navigate an uncertain economy.

600450

600450

Add new comment