Date: 17 December 2025

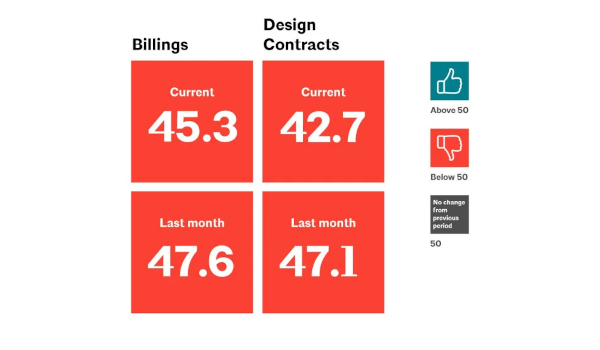

Inquiries into new projects only increased modestly this month, and the value of newly signed design contracts continued to soften. Firms are unlikely to see a significant increase in billings until work in the pipeline resumes.

“Weakness in business conditions at architecture firms continues to be widespread, with declining billings across all major specializations and in every region except the Midwest,” said Kermit Baker, PhD, AIA Chief Economist. “However, inquiries for new projects continued to increase, and design activity at firms in the Midwest – a region that traditionally has had a disproportionate share of manufacturing activity – appears to have hit its bottom for this cycle and is expected to continue to improve.”

Key ABI highlights for November include:

• Regional averages: Midwest (52.3); South (46.1); West (43.6); Northeast (43.1)

• Sector index breakdown: institutional (47.6); multifamily residential (46.6); commercial/industrial (45.2); mixed practice (firms that do not have at least half of their billings in any one other category) (44.5)

• Project inquiries index: 51.4

• Design contracts index: 42.7

The regional and sector categories are calculated as three-month moving averages and may not always average out to the national score.

Access resources to help architects successfully navigate an uncertain economy.

600450

600450

Add new comment